The "standout" markets of Perth, Adelaide, and Brisbane have driven national housing market performance in 2024, noted Domain’s 2024 End-of-Year Wrap and 2025 Outlook report.

Chief of research and economics Nicola Powell said that, despite ongoing cost-of-living pressures and a persistently high cash rate, the market showed an impressive ability to adapt.

"What was expected to be a year of rate cuts became a testament to the strength of demand and undersupply that's dominating and continues to push prices up," Dr Powell said.

She expects the mid-sized capitals to continue to lead price growth in 2025, but at a slower pace.

House and unit price forecasts to the end of 2025

“In 2025, we expect prices to keep rising but at a slower pace than in 2024, due to affordability pressures and more buyer options, giving Australians greater leverage as the year unfolds,” Dr Powell said.

| Location | House | Unit |

|---|---|---|

| National | +4% to 6% | +3% to 5% |

| Sydney | +4% to 6% | +4% to 6% |

| Melbourne | +3% to 5% | -2% to 0% |

| Brisbane | +5% to 7% | +7% to 9% |

| Perth | +8% to 10% | +8% to 10% |

| Adelaide | +7% to 9% | +7% to 9% |

| Canberra | +3% to 5% | -4% to -2% |

| Combined capitals | +5% to 7% | +3% to 5% |

| Regional NSW | +2% to 4% | +1% to 3% |

| Regional Vic | -5% to -3% | -2% to 0% |

| Regional Qld | +6% to 8% | +5% to 7% |

| Combined regionals | +2% to 4% | +2% to 4% |

Source: Domain '2024 End-of-Year Wrap and 2025 Outlook' report.

For reference, Domain's previous outlook report tipped house prices across Australia to rise by 4% to 6% in 2024 – a prediction that came true.

Speaking to the Savings Tip Jar podcast in December 2023, Dr Powell said Sydney property prices would lead the nation, suggesting the uptick experienced in Perth, Brisbane, and Adelaide came as a surprise.

2025: tale of two halves

The forecast for next year is expected to be a ‘before and after’ story, marked by an anticipated mid-year cut to the cash rate.

“The first half will be weaker as the dynamics of 2024 carry over, while the second half should see a rebound, with the Reserve Bank of Australia potentially moving to cut the cash rate which would serve as a strong catalyst to drawing more buyers back to the market,” Dr Powell said.

Dr Nicola Powell, Domain Chief of Research and Economics

See also: ANZ economists expect 'later and shallower' easing cycle

An interest rate cut is singled out as the number one likely driver of 2025 housing market trends, with the report finding it may take one or two rate cuts to spur buyers into action.

The report also tips housing to be a key battleground issue in the 2025 federal election, due by mid-May, and forecasts increased housing density in middle-ring suburbs in Sydney, Melbourne, and Brisbane – a bid to ease housing shortage and affordability issues.

Pools still rule

In reviewing Domain data for 2024, the report found ‘pool’ remained the top search term among Australian property watchers, suggesting buyers are still looking for home luxuries despite affordability concerns.

See also: How much does it really cost to install a swimming pool in Australia?

‘Waterfront’ and ‘view’ took the second and third spot nationally and searches for ‘study’ dropped to seventh place, down from second in 2023.

The report concluded this indicates a shift in the work-from-home trend as more workers returned to the office.

The search term ‘granny flat’ held steady in fourth place, reflecting tight rental markets, a growing interest in side incomes, additional workspaces, or multigenerational living, the report suggested.

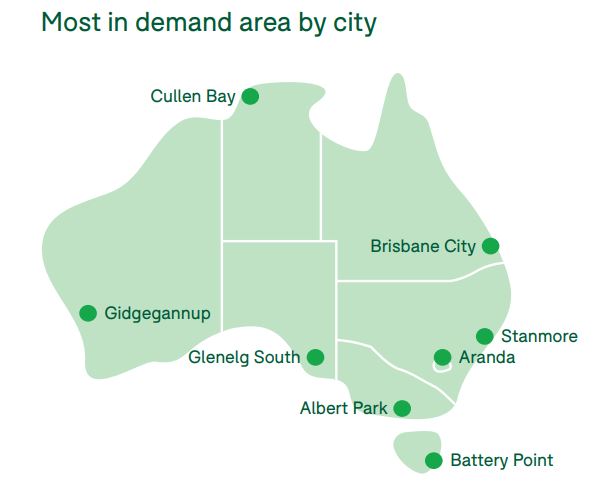

The snapshot below outlines the most in-demand suburbs by city:

Source: Domain

The Sydney, Melbourne, Adelaide, and Perth markets continued to generate a significant number of enquiries for regional tree and sea changes.

However, interest in regional property declined in Sydney and Melbourne and increased in Adelaide and Perth.

Distressed listing hot spots

The report also noted suburbs with the highest proportion of distressed listings in capital cities and regional Australia.

In property terms, 'distressed listings' are those where owners are forced to sell due to facing mortgage stress or are desperate to sell for other reasons.

Domain identifies distressed listings via a machine-learning model that flags when a seller seeks an urgent sale, with the percentage expressed as a proportion of total listings in a given suburb.

| City | Highest Distressed Listings |

|---|---|

| Sydney | Blacktown (13.9%) |

| Melbourne | Casey (4.2%) |

| Brisbane | Sunnybank (18.4%) |

| Adelaide | Port Adelaide - West (2%) |

| Canberra | Belconnen (1.8%) |

| Perth | Canning (3.8%) |

| Hobart | Sorrell - Dodges Ferry (2%) |

| Darwin | Darwin City (5.1%) |

| Regional Australia | Gold Coast - North, Qld (12.2%) |

Source: Domain

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Additional Repayments | Split Loan Option | Tags | Row Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.79% p.a. | 5.83% p.a. | $2,931 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | |||||||||||

5.74% p.a. | 5.65% p.a. | $2,915 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | |||||||||||

5.84% p.a. | 6.08% p.a. | $2,947 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure |

")

Main image by Larry Snickers via Pexels

Image of Dr Powell, supplied

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Harrison Astbury

Harrison Astbury

William Jolly

William Jolly