It's the 19th consecutive month of home price increases with the August figure coming in higher than the revised 0.3% growth for July, according to CoreLogic figures.

But the pace of growth continues to slow with the quarterly increase in national property values now less than half the growth rate in the same quarter of 2022.

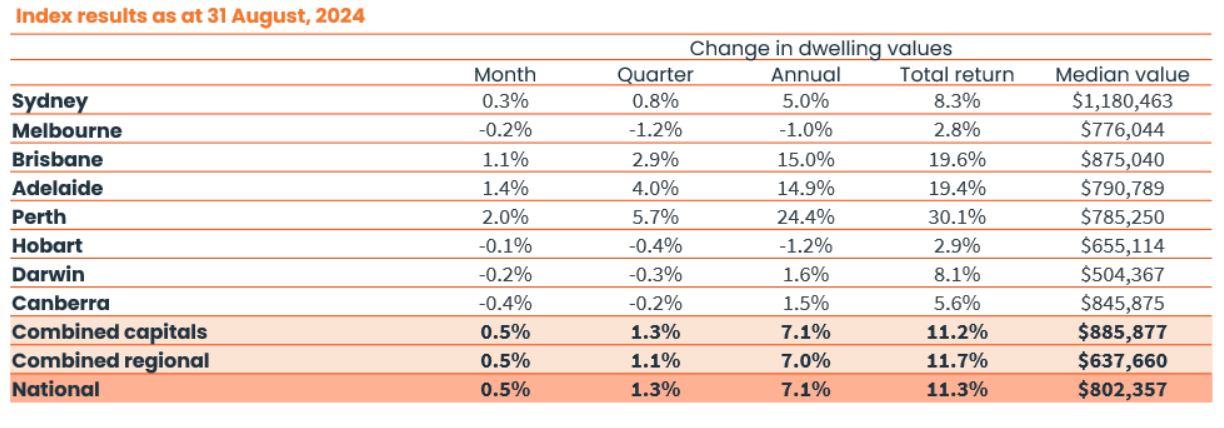

Capital city disparity

Perth led the increase in monthly gains with a 2% jump in August, followed by strong gains in Adelaide (1.4%) and Brisbane (1.1%).

Both Perth and Adelaide have now also jumped Melbourne in recording higher median home values.

The Victorian capital was notably overtaken by Brisbane in January 2024.

Melbourne's median value of $776,044 now ranks behind Sydney, Brisbane, Canberra, Adelaide, and Perth.

It's the first time Perth's median home value has been higher than Melbourne's since February 2015 when Western Australia was coming off an iron ore boom.

It's also the first time in CoreLogic's 40-year history of collecting median dwelling data that Adelaide has a higher median home price than Melbourne.

Source: Hedonic Home Value Index for August 2024

Source: Hedonic Home Value Index for August 2024

Why is Melbourne's property market stagnating?

CoreLogic analysts noted media dwelling values are highly skewed by the portion of units in each market.

Melbourne's median is weighed down by the composition of housing where around a third of the homes are units, compared with around only 16% of homes in both Perth and Adelaide.

But CoreLogic's head of research Eliza Owen said that there were other factors contributing to Melbourne's softer market conditions.

She noted a fall in demand among investors in Victoria linked to land tax changes looked to be having some effect.

ABS lending data shows a falling number of investment loans in the state following last year's state government decision to widen the tax net for investment property owners.

Victorian landlords and holiday home owners now have to pay land tax on property values kicking in at $50,000.

It's effectively seen another 380,000 investors paying land tax for the first time.

Ms Owen said interstate migration had also been weaker in Victoria, Tasmania, and the ACT in recent years contributing to declines in price growth in those markets.

Seasonal factors

Growth eased in most capital cities through winter with Brisbane having the most pronounced slowdown in its quarterly growth rate, recording 4.1% in May compared to 2.9% in August.

Ms Owen said that while seasonal factors may have contributed to weaker growth through winter, affordability constraints are also a key variable.

"The seasonally adjusted Home Value Index had a stronger result through the three months to August at 1.7%," she said.

"But this is still down from the 3.3% lift seen in the winter of 2023."

Ms Owen said the high levels of growth in Perth, Adelaide, and Brisbane would be difficult to sustain.

"Housing values cannot keep rising at the same pace in the mid-sized capitals of Perth, Adelaide and Brisbane when affordability is becoming increasingly stretched, particularly in the context of elevated interest rates, loosening labour market conditions and cost of living pressures."

Buyers looking to 'cheaper' markets

Prices in the least expensive quartile of home prices in the combined capital city market continue to rise at a much higher rate than more expensive homes.

Home values in the lowest 25% grew 2.7% in the quarter ending August, compared to just 0.3% in the upper quartile.

In another sign buyers are looking for affordable housing, the quarterly change in unit values was higher than house values in five of the eight capital cities.

CoreLogic singled out more affordable pockets of the national housing market where prices have leapt considerably in the past year.

They include:

Canterbury in Sydney (up 13.3%)

Kwinana in Perth (up 31.4%)

Springwood-Kingston in Brisbane (25.5%)

Advertisement

Buying a home or looking to refinance? The table below features home loans with some of the lowest interest rates on the market for owner occupiers.

| Lender | Home Loan | Interest Rate | Comparison Rate* | Monthly Repayment | Repayment type | Rate Type | Offset | Redraw | Ongoing Fees | Upfront Fees | Max LVR | Lump Sum Repayment | Additional Repayments | Split Loan Option | Tags | Row Tags | Features | Link | Compare | Promoted Product | Disclosure |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

5.79% p.a. | 5.83% p.a. | $2,931 | Principal & Interest | Variable | $0 | $530 | 90% |

| Promoted | Disclosure | |||||||||||

5.74% p.a. | 5.65% p.a. | $2,915 | Principal & Interest | Variable | $0 | $0 | 80% |

| Promoted | Disclosure | |||||||||||

5.84% p.a. | 6.08% p.a. | $2,947 | Principal & Interest | Variable | $250 | $250 | 60% |

| Promoted | Disclosure |

")

Image by Dillon Kydd on Unsplash

Ready, Set, Buy!

Learn everything you need to know about buying property – from choosing the right property and home loan, to the purchasing process, tips to save money and more!

With bonus Q&A sheet and Crossword!

Harry O'Sullivan

Harry O'Sullivan

Brooke Cooper

Brooke Cooper