.jpg)

The federal government is preparing to ban debit card surcharges from 1 January 2026, subject to a review currently underway by the Reserve Bank of Australia (RBA).

The RBA announced on Tuesday it's launching a review into retail payments regulation, examining the costs merchants face when they accept card payments and the current framework for surcharging.

Australian consumers are estimated to pay around $1.5 billion a year on debit and credit card surcharges although some industry estimates put the figure at more than double that amount.

The government's planned action will only ban debit card fees and not extend to credit card surcharges at this stage.

RBA critical of fee regime

The RBA has long had its eye on excessive card payment processing fees in Australia and on Tuesday, released an Issues Paper, inviting feedback on the current regulatory framework and suggested regulatory changes.

In March 2024, it warned it would impose new regulations on banks if they failed to address excess card surcharges being passed on to both consumers and merchants.

Under current regulations, retailers can pass on payment processing costs to consumers paying by card, but they are not allowed to profit from it.

While many larger businesses continue to absorb card surcharges or negotiate favourable terms with payment platforms, many smaller operators pass the fees onto their customers.

However, the RBA acknowledges current regulations have failed to keep up with how the payments industry has evolved.

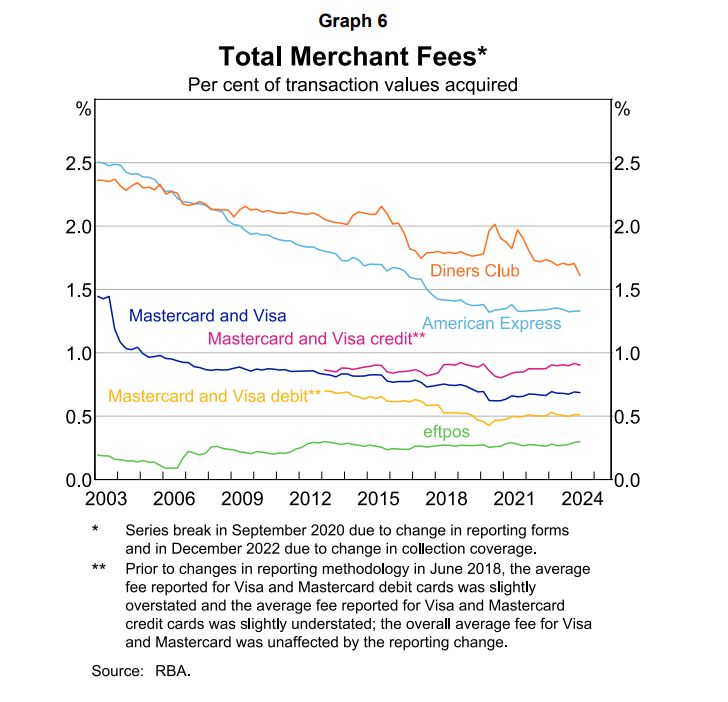

The table below illustrates fees charged by various card providers as a percentage of transaction values over the past two decades:

RBA research in 2022 found the average cost to a merchant when accepting Eftpos was 0.3% of the transaction; Mastercard or Visa was 0.5% for debit and 0.9% for credit; and Amex was much higher at 1.3%.

Fees can also differ based on if a customer taps or inserts, or selects Cheque or Savings, or Credit.

Certain product lines also face different merchant costs, such as if it's a platinum product.

Consumers have increasingly adopted debit cards for tap-and-go payments which, in theory, should incur lower payment processing fees but these can be subject to so-called blended pricing models.

Under these payment plans, merchants pay the same processing fee to the bank or payment provider regardless of the card the consumer uses.

Consumers are also often hit with an all-encompassing flat fee for using a card even if it incurs a lower processing cost.

The latest Reserve Bank issues paper notes payment providers are increasingly bundling their services, effectively leading to higher fees that are then passed onto consumers as payment surcharges.

The RBA had previously urged banks to speed up the adoption of least-cost routing (LCR), a scheme that automatically routes card payments through the lowest-cost channel rather than a one-size-fits all charge.

In most cases, this is Eftpos in cases where the bank or card has enabled this.

As at June 2024, large providers had enabled LCR for 70% of their merchant customers for in-person transactions, according to RBA data.

Uptake for online transactions has been much slower, the paper notes.

Government keen to act

The federal government has jumped ahead of the RBA with its plan to ban surcharges on debit transactions although the suggestion is canvassed in the RBA issues paper.

However, the RBA's review goes further, seeking submissions on the possibility of banning all card surcharges such as in the European Union and the United Kingdom.

The federal government has also reportedly committed $2.1 million in extra funding to the Australian Competition and Consumer Commission to monitor card surcharges in the marketplace.

The RBA has called for written submissions to its review by 3 December.

Image by Blake Wisz on Unsplash

Harrison Astbury

Harrison Astbury

Denise Raward

Denise Raward

Harry O'Sullivan

Harry O'Sullivan

Hanan Dervisevic

Hanan Dervisevic